Singapore is one of the developed countries with the lowest tax rates in the world, often recognized as a "global legal tax haven." The low tax rates and favorable tax policies, along with a stable and safe living environment, are why Singapore is one of the top global choices for overseas investment and immigration. The maximum rate for corporate income tax in Singapore is 17%, the maximum personal income tax rate does not exceed 22%, and there are no capital gains or inheritance taxes.

I Who Needs to Pay Taxes

1 Singapore citizens and individuals who have settled and become permanent residents of Singapore;

2 Non-citizens or non-permanent residents who meet any of the following criteria:

(1) An individual who has stayed or worked in Singapore for at least 183 days in a calendar year is considered a tax resident of Singapore for that year;

(2) An individual who has continuously stayed or worked in Singapore for three consecutive calendar years is considered a tax resident of Singapore for each of those years.

II How Much Income is Taxable

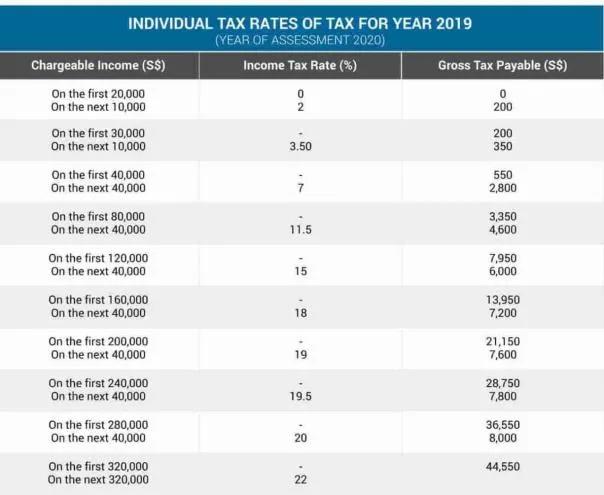

The personal income tax threshold is SGD 20,000. Residents with income below this threshold do not need to pay personal income tax, and those earning more than SGD 20,000 are subject to a progressive tax system:

Note: Residents earning less than SGD 20,000 annually do not need to pay tax but are still required to file a return.

For example: If a bus driver in Singapore earns a monthly salary of SGD 2,200, their annual total income would be SGD 2,200 * 12 = SGD 26,400. According to the tax rate chart below, the first SGD 20,000 is tax-free, and the tax payable on the remaining SGD 6,400 (SGD 6,400 * 2%) is SGD 128. Therefore, the actual tax amount payable is SGD 128.

III Do You Need to File Taxes Proactively?

Initially, IRAS will determine if you need to file taxes based on internal records.

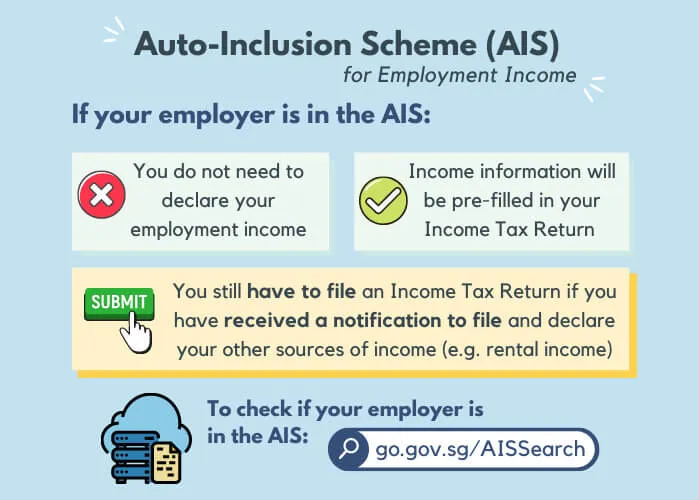

If you only have employment income and your employer is part of the Auto-Inclusion Scheme (AIS), then you may be eligible for the No-Filing Service (NFS). A simple way to know is if you did not receive a tax filing notice, you are already included in the NFS, and you only need to wait to receive your tax bill and pay the taxes by the due date.

Additionally, you need to log into the IRAS website https://www.iras.gov.sg/, use SingPass to access MyTax Portal to check if your Notice of Assessment (NOA) or the information on your tax bill is correct and confirm it.

Even if you are in the following two situations, you still need to confirm:

1 You had no income in the previous year;

2 You have only employment income, and your employer is part of the AIS and has already submitted your employment income details to IRAS.

Self-employed individuals or tax residents with additional income (such as rental income) must log into the IRAS website to declare their extra income.

IV How to File Taxes

Personal income tax in Singapore can be filed via paper filing or electronically. Paper filings need to be submitted by April 15; electronic filings must be completed by April 18.

To file personal income tax online, log into the IRAS website at http://www.mytax.iras.gov.sg and submit the required information online.

Note: To prevent identity theft, the website uses SingPass two-factor authentication. You must enter two passwords: your fixed password and a one-time password generated by the password generator.

V How to Pay Taxes

After filing, taxpayers will receive a tax bill (Notice of Assessment, NOA) from IRAS between April and September. Once you receive the NOA, check it carefully. If there are any errors, you can object to IRAS within 30 days from the date shown on the NOA. If there are no objections, the tax due must be paid within one month of receiving the NOA; otherwise, penalties may apply.

You can choose any of the following payment methods:

1 SAM machines

2 AXS machines or the AXS APP

3 ATMs (POSB/DBS, OCBC)

4 Check/GIRO/Online Transfer

Note: It is recommended to set up GIRO for interest-free monthly installments to alleviate the burden of lump-sum payments and to avoid penalties for forgotten tax payments.

VI Tax Reduction Programs

In recent years, the Inland Revenue Authority of Singapore has introduced the Auto-inclusion Scheme (AIS). If a company has joined the AIS, it no longer needs to distribute tax forms such as IR8A/IR8S to employees in the traditional way. By March 1 each year, employers only need to submit their employees' income information electronically in the format required by IRAS.

From the fiscal year 2021, employers with six or more employees must participate in AIS.

If your company has not yet participated in the Auto-Inclusion Scheme (AIS), please contact us. Our professional team is dedicated to serving you!

By filing, we can assist taxpayers with tax relief and tax rebate, helping to reduce their burden. This includes reliefs for childbearing, pursuing further education, living with parents, and hiring domestic helpers. Specifically, this includes:

Tax Relief Scope One: Child-rearing

1 Qualifying Child Relief (QCR): Agreed upon by both parents or enjoyed by one parent, deductible up to SGD 4,000 per child; for disabled children, the deductible amount is SGD 7,500.

2 Working Mother's Child Relief (WMCR): Only applicable to working mothers, with the first child's deduction at 15% of income, the second child at 20%, and from the third child onwards at 25%. The total deduction percentage accumulates, capped at 100% of the working mother's income.

3 Grandparent Caregiver Relief (GCR): Working mothers who entrust their children aged 12 or under to their own or their spouse's parents or grandparents can apply for a rebate of up to SGD 3,000.

4 Parenthood Tax Rebate (PTR): Deducted from the taxpayer's actual tax payable; if not fully used, it can be carried forward. The first child gets a rebate of SGD 5,000, the second child SGD 10,000, and from the third child onwards, SGD 20,000 each.

5 Foreign Maid Levy Relief: Available to married female taxpayers, the deductible amount is double the maid levy paid by the taxpayer or her husband in the previous year. Available even without children.

Tax Relief Scope Two: Caring for Relatives

1 If the taxpayer supported his or her spouse's parents or grandparents residing locally last year, they can enjoy Parent Relief provided the elder is at least 55 years old or disabled (physically or mentally), and their income does not exceed SGD 4,000.

2 If living with parents, the deduction amount is SGD 9,000; if not living with parents, the amount is SGD 5,500. If the parent is disabled and living with the taxpayer, the deduction amount is SGD 14,000; if not living together, it is SGD 10,000. A taxpayer can receive Parent Relief for up to two people.

3 Besides parents, taxpayers supporting a spouse earning less than SGD 4,000 last year are eligible for Spouse Relief of SGD 2,000. If the spouse is disabled, the deduction amount is SGD 5,500.

4 If the taxpayer supported his or her own or spouse's disabled siblings last year, or if they lived together, each can grant the taxpayer Handicapped Brother/Sister Relief of SGD 5,500.

5 Additionally, taxpayers who topped up the CPF accounts of their spouse, siblings, their own or their spouse's parents, and grandparents last year, as long as they did not reach their Full Retirement Sum, can enjoy a maximum deduction of SGD 7,000, which will automatically reflect on the tax form.

Tax Relief Scope Three: Educational Courses and Work Expenses

Course Fees Relief: For instance, if the taxpayer attended a course or seminar last year and obtained a qualifying academic or professional certification, they can claim some work expenses, such as entertaining clients, if not reimbursed by the employer. It is essential to keep receipts and records for verification.

Tax Relief Scope Four: Retirement Planning and Life Insurance

Taxpayers who deposited cash into the Supplementary Retirement Scheme (SRS) last year can enjoy a tax deduction equal to the amount deposited, up to a maximum of SGD 15,300 per year.

If the taxpayer paid less than SGD 5,000 in CPF last year, they can claim a deduction for life insurance premiums paid by themselves or their spouse last year. The specific deductible amount depends on the difference between the CPF contribution and SGD 5,000, and 7% of the insured amount or the premiums paid, whichever is lower.

Tax Relief Scope Five: Donations or Donated Items

Donations to charities approved by the authorities are eligible for a deduction of 2.5 times the donated amount. Charities will record the taxpayer's ID number and other information and notify IRAS directly; the related deduction will automatically reflect on the tax form.

Besides cash donations, donations of stocks, antiques, artworks, and real estate are also eligible for tax deductions, as long as the relevant authorities appraise these items.