The corporate income tax rate in Singapore is 17%. Capital gains (e.g., revenue from the sale of fixed assets, foreign exchange gains from capital transactions, etc.) are not taxed. Compared to other countries, Singapore's corporate tax has significant advantages.

I. Tax Filing Deadline

Unlike China, the start and end dates of the fiscal year in Singapore can be any month. It is usually calculated from the month of company registration and ends after one full calendar year. The tax filing deadline is typically November 30 of the following calendar year. For example, for the fiscal year 2021, the corporate income tax filing deadline is November 30, 2021.

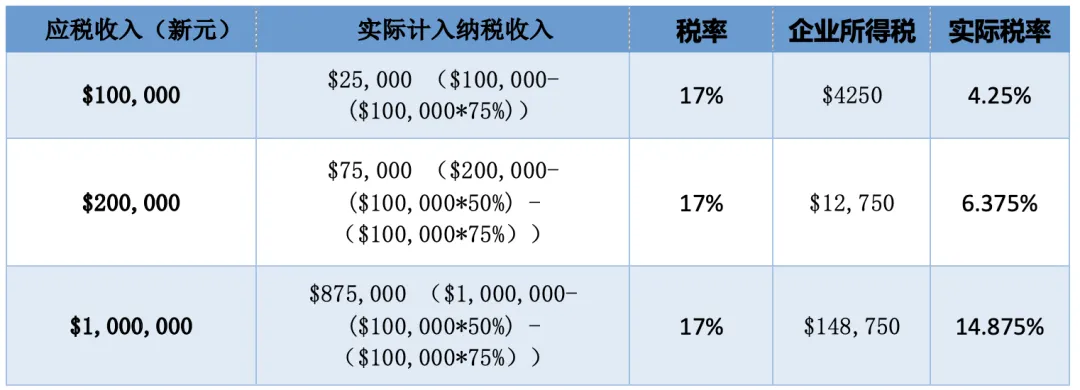

If a company was established on January 1, 2021, the Accounting and Corporate Regulatory Authority (ACRA) of Singapore allows the first fiscal year to be up to 24 months, but we generally recommend clients to set it at 12 months, that is, to close accounts on December 31, 2021. This maximizes the benefit of tax incentives provided by the Inland Revenue Authority of Singapore (IRAS) for newly registered companies for the first three years (with 12 months counting as one tax year). Specifically, for the first three years, 75% of the first SGD 100,000 of profits can be tax-free. For more details on tax incentives for start-up companies, refer to section D-1: Tax Exemptions and Relief for Small Start-up Companies.

II. Income Tax Calculation

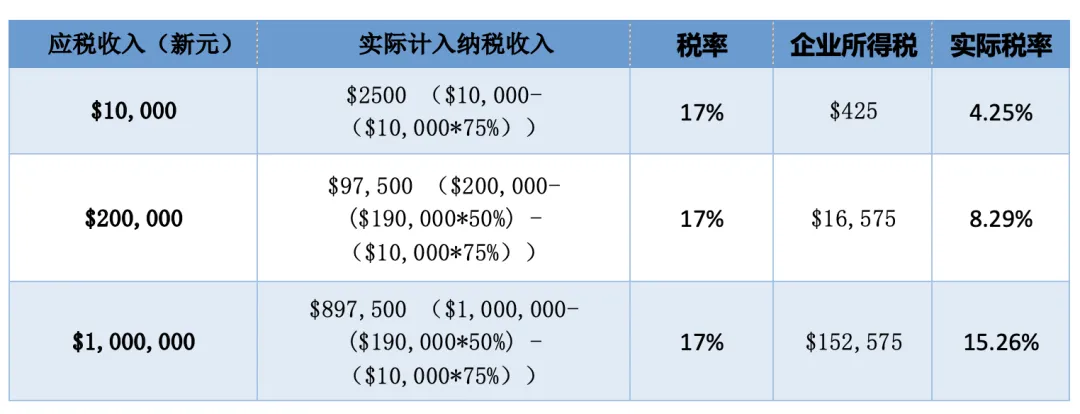

The corporate income tax rate in Singapore is 17%. However, the Singapore government values support for small and micro enterprises, and the effective tax rate for low-income small and micro enterprises is far lower than 17%. According to the latest policy for 2020, the first SGD 10,000 of taxable income is eligible for a 75% exemption, and income between SGD 10,000 and SGD 200,000 is eligible for a 50% exemption.

Additionally, Singapore enterprises enjoy various other tax incentives and reliefs, which will be detailed below.

III. Estimated Chargeable Income (ECI)

According to the IRAS, starting from the financial year 2020, all companies must file an Estimated Chargeable Income (ECI). What is ECI, and when is it required to file ECI?

The fiscal year in Singapore is usually calculated from the month of company registration and ends after one full calendar year. The tax filing deadline is typically November 30 of the following calendar year.

After the end of the fiscal year, a company must generate financial statements and hold an annual general meeting (AGM) where all shareholders sign the company's financial report. Typically, within one month after the AGM, the company must submit its financial statements to ACRA for the annual return filing.

Tip: If your company is not profitable and the annual revenue is less than SGD 5 million, there is no need to file an ECI. Note that the ECI is only an estimate and not the final tax return.

The IRAS will issue an ECI form to the company, which must be submitted within three months. Based on the information provided, IRAS will issue a tax return form, which the company must complete and submit along with supporting documents (e.g., financial statements, audit reports).

The IRAS will then assess the tax payable and issue a tax bill. The company must pay the tax according to the bill amount, thus completing the tax filing process.

IV. Tax Incentives and Reliefs

All enterprises, whether local or foreign, must pay taxes on income earned in Singapore and overseas income received in Singapore according to the law. Singapore distinguishes between resident companies and non-resident companies for tax purposes.

Resident companies enjoy more tax incentives and reliefs.

Criteria for Resident and Non-resident Companies:

1 Resident Company: A company is considered a Singapore resident if its control and management are in Singapore, regardless of whether it is registered under Singapore law.

2 Non-resident Company: A company is considered non-resident for tax purposes if its control and management are not in Singapore, even if it is registered in Singapore.

A. Tax Exemptions and Relief for Small Start-up Companies

For small start-up companies, the Singapore government offers a 75% tax exemption on the first SGD 100,000 of income and a 50% exemption on the next SGD 100,000.

Any newly registered company that meets the following conditions is eligible for tax exemptions in the first three years:

1 Incorporated in Singapore.

2 Subject to Singapore's personal income tax system.

3 Has no more than 20 shareholders, with at least one holding 10% or more of the shares.

4 Not primarily an investment holding company;

5 Not engaged in property development, investment, or sales.

B. Loss Carry-back Relief

To assist companies in coping with cash flow problems due to economic downturns, the government introduced an enhanced loss carry-back relief in the 2020 Budget. This allows companies to carry back qualifying deductions for the 2020 tax year to the three previous tax years for a tax refund.

The maximum limit for this relief is SGD 100,000.

C. Avoidance of Double Taxation Agreements (DTA)

Singapore tax resident companies may face double taxation if their foreign-sourced income is taxed overseas and then remitted to Singapore.

Singapore has signed over 20 free trade agreements (FTA) and 74 comprehensive and 8 limited double taxation avoidance agreements (DTA) to mitigate double taxation.

Singapore tax residents earning income from other countries can apply to IRAS for a Certificate of Residence (COR). A COR is a letter certifying that the company is a Singapore tax resident. Tax residents need this certificate to claim relief under the DTA signed between Singapore and other jurisdictions to avoid double taxation.

Additionally, the first SGD 200,000 of R&D expenses incurred by Singapore companies can be partially deducted from taxable income. Various incentives such as basic deductions, additional deductions, enhanced deductions, research and development tax credits, and start-up R&D tax incentives are available.